Essex Global Environmental Opportunities Strategy (GEOS) – Review and Outlook

First Quarter ended March 31, 2026

The most important catalysts for clean technology which drove clean tech listed equity performance last year, rising power demand and geoeconomic fragmentation are not only intact but have strengthened during the first quarter of 2026. The Essex Global Environmental Opportunities Strategy (GEOS) invests in infrastructure and industrial technologies that can power the energy transition and the world’s efficiency upgrade. GEOS focuses on companies that cut costs, boost reliability and increase throughput across power, water, transport and industry. Our focus is to invest in companies that enable the transition in real-world systems, and the Iran conflict further places a premium on these catalysts. We must diversify our energy supplies to lessen economic and social harm while enabling economic growth with enhanced productivity. The timing could not be better, as pricing for solar and battery storage is at all-time lows, much cheaper than natural gas, with other competitive advantages such as speed to market. This could not come at a better time – the proverbial power switch is on. This switch extends beyond clean power, to clean resources and clean mobility and systems. Building generation capacity alone is not enough. The real opportunity lies in efficiency – technologies that help economies with production while using less energy.

Performance and Transactions

For the first quarter of 2026 ending March 31, the Essex Global Environmental Opportunities Strategy (GEOS) returned 0.68% (0.43% net), versus -2.99% for the iShares MSCI World ETF (URTH). The Wilderhill Clean Energy Index[1] posted 3.5% for the first quarter. For the trailing twelve months ended March 31, GEOS returned 35.31% (34.0% net) versus 19.4% for URTH and 102.0% for the Wilderhill.

Contribution to first quarter performance was led by Amprius Technologies (AMPX), the battery technology company focused on silicon anodes, which enable superior charging cycle life with twice the energy of current offerings. Amprius has over 500 current customers across several end markets, with the most commercial uptake now in drone applications. AMPX achieved profitability and positive free cash flow in 2025 and is guiding over 70% revenue growth this year. We initiated our position in June of last year at 1%, and the current weight is over 2% due to stock price appreciation. Nextpower (NXT) was a top performance contributor, offering solar and storage solutions for utility scale projects. NXT provides systems design and software to optimize power output, their legacy solar trackers and new offerings such as electrical balance of systems solutions. We initially purchased NXT in September of 2025 at 1.5%, with the weight growing to over 2.5% at quarter-end given stock price performance. Long-term holding and machine vision systems firm Cognex (CGNX) posted strong contribution on news it increased new customer accounts at three times the rate of 2024. We added to the position in June and July of last year, and trimmed on price strength in late February. Rounding out the top contributors for the first quarter is GE Vernova (GEV) which GEOS has held since April of 2024. GEV offers a broad suite of power offerings, from natural gas and wind turbines to large and small form nuclear and solar power. We added to GEV early in the year on price weakness, and the shares strengthened in price for the remainder of the quarter as sentiment improved on the base fundamentals of increased domestic power demand.

The top detractor of GEOS performance for the first quarter was the German logistics and factory automation firm Kion Group (KGX.GY), with share price weakness based on perceived pricing pressure and customer order delays. We exited our position in Kion late in March. Stationary battery storage company Fluence Energy (FLNC) was initially purchased last year in August and was a top performer for 2025 but share price appreciation languished after fourth quarter earnings suggested poor bookings conversion to revenue as well as pricing compression. First Solar (FSLR) was a performance detractor as its earnings results missed expectations due to weak revenue and profitability and poor revenue guidance for 2026. We sold FSLR in early March to fund a new position in European solar inverter company SMA Solar Technology (S92 GY), as demand for utility scale solar improves in the EU amidst spiking natural gas prices. Finally, Energy Recovery (ERII) was weak for the quarter given a revenue miss on delays for large scale desalination plant construction in the Middle East. Our assessment is these projects should unfold and lead to revenue later in 2026. ERII has renewed focus on energy recovery solutions for desalination, their core market, as they exit end markets where success is not at hand, such as refrigeration.

Lindsay (LNN) is a new GEOS position, added early in the quarter on the prospect their core business, smart irrigation will improve this year from the sub-par growth of the past several years. Deere (DE) was used as the source of funds, as we see more relative growth in LNN for the year. In late January we initiated a position in Alfen N.V. (ALFEN NA), the Netherlands-based smart grid firm with almost 100% revenue exposure to the EU. Alfen has been providing transformers for industrial applications since 1960 and is now a leader in stationary battery storage and EV charging solutions, as well as their legacy transformer business. Another new position for GEOS is SOLV Energy (MWH), the largest solar engineering, procurement and construction (EPC) firm in North America, with an install base of over 18 gigawatts (GW) in 34 states. MWH has a strong, experienced management team, and was founded in 2008. Other new positions include Sprouts Farmers Market (SFM) in the GEOS low carbon commerce theme and Ambiq Micro (AMBQ). Ambiq offers ultra-low power semiconductor platforms and solutions for battery-powered AI devices in applications such as predictive maintenance in factory automation or field conditions monitoring in agriculture. AMBQ solutions enable devices to operate at the network edge versus in the cloud, leading to lower power consumption and enhanced response rates. Sprouts shares were purchased in March after the stock was overly punished on consumer spending fears, and we believe the growth to valuation is currently attractive. Sprouts operates almost 500 stores in 25 states, with a business model that leverages local distribution and smaller square footage to optimize costs with differentiated grocery offerings.

Outlook

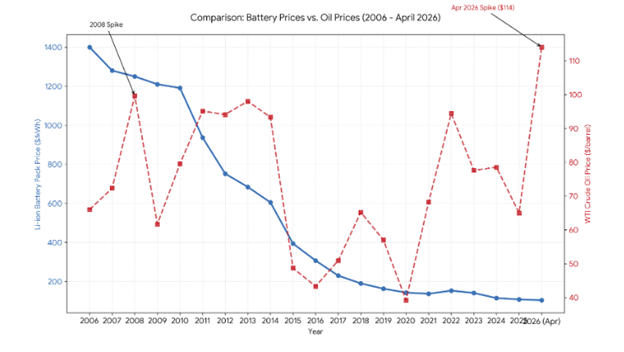

Without power and water economic growth is impossible. GEOS invests across nine themes, that can be categorized as clean power, clean mobility & systems and clean resources, which enable economic growth while lowering risks and optimizing inputs such as energy. The global trends and risks that have been catalyzing the benefits of clean technology exploded with the conflict in Iran, demonstrating the grave consequences when our economy is reliant on oil, a traded commodity with pricing volatility that always spikes during global geopolitical conflicts. The chart below depicts the long-term volatility of oil versus lithium-ion battery prices:

Source: IEA, BNEF, Essex, 4/26

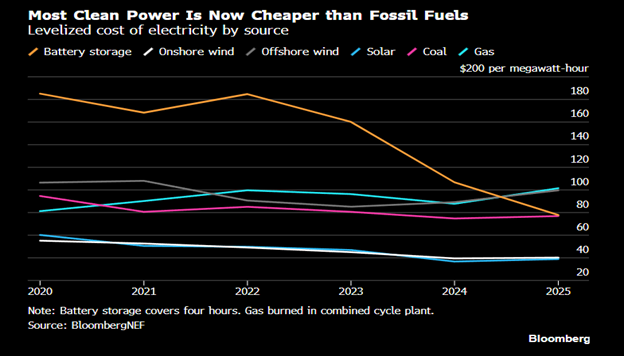

The oil price spike of 2008 was driven by the rapid global commodity price spikes as China and India entered the world stage of economic growth. Oil price pressure in 2013 was due to the Arab Spring, which impacted fears of closure of the Suez Canal and the Sumed Pipeline, both critical choke points for oil trade, which were exacerbated later in the year by sanctions in Iran and the Syrian Civil War. Sound familiar? As oil is a globally traded commodity, with marginal demand and speculation driving pricing, commodity risk directly impacts our economic growth and social welfare. Contrast oil with global battery prices which follow physics, exhibiting learning curves and subsequent technological adoption – a distributed resource where electrons can be stored and harvested as needed, locally, limiting global trading risks and our need to deploy military forces with civil and economic casualties. Physics matters, impacting economics and for this reason clean power is cheaper than fossil fuels:

This is science, and is now we believe a national competitive advantage which the EU recognized at the start of the Ukrainian War and is re-embracing now as oil and natural gas prices spike.

The drivers for clean tech going into 2026 were driven by geo-economics, such as onshoring or tariff structures placing premiums on productivity and industrial efficiency – doing more with less amidst pricing pressures. The data center and AI electron hunger brought to light the need for more power now, with greater efficiency. This, even before the conflict with Iran. We believe that amidst uncertainty, the economies and companies which invest in technologies and services that enhance efficiency and productivity will outcompete and lead. We believe every holding in GEOS enables doing more with less, from water management systems to advanced battery chemistry, solar arrays and electric grid monitoring. The switch is on – the time is now.

Disclosures

This commentary is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. The opinions and analyses expressed in this commentary are based on Essex Investment Management LLC’s (“Essex”) research and professional experience and are expressed as of the date of its release. Certain information expressed represents an assessment at a specific point in time and is not intended to be a forecast or guarantee of future results, nor is intended to speak to any future periods. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties.

This does not constitute an offer to sell or the solicitation of an offer to purchase any security or investment product, nor does it constitute a recommendation to invest in any particular security. An investment in securities is speculative and involves a high degree of risk and could result in the loss of all or a substantial portion of the amount invested. There can be no assurance that the strategy described herein will meet its objectives generally or avoid losses. Essex makes no warranty or representation, expressed or implied; nor does Essex accept any liability, with respect to the information and data set forth herein, and Essex specifically disclaims any duty to update any of the information and data contained in the commentary. This information and data does not constitute legal, tax, account, investment or other professional advice. Essex being registered by the SEC does not imply a certain level of skill or training.

[1] The Wilderhill Clean Energy Index (ticker: ECO) is a modified equal dollar weighted index comprised of publicly traded companies whose businesses stand to benefit from societal transition toward the use of cleaner energy and conservation.

Please find important disclosures here